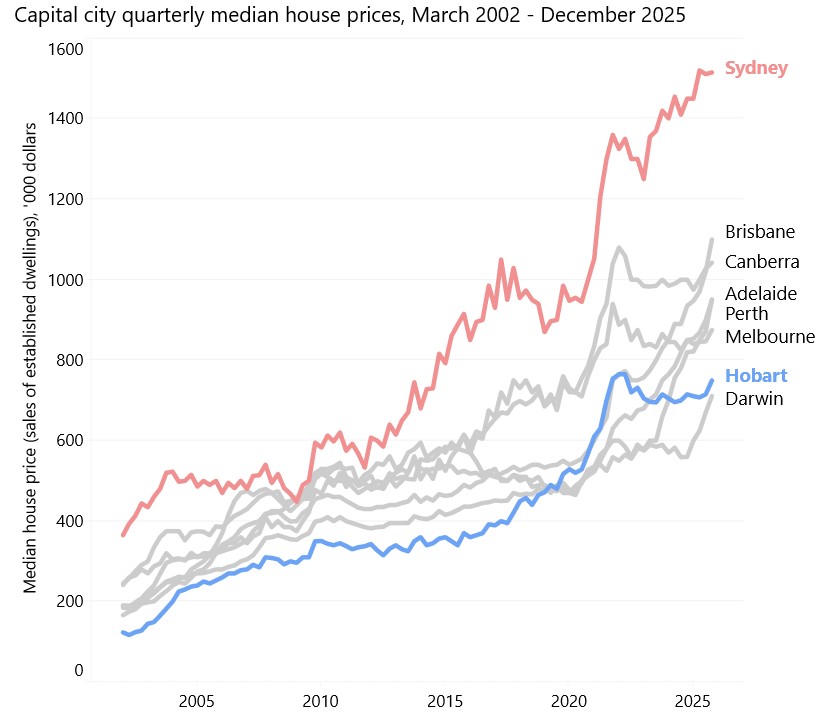

time, house prices have skyrocketed. Late last year, the median house

price in Hobart was

$749,500 – double what it was a decade ago and increasingly out of reach for many Tasmanians.

The reforms

After years of debate, the profits made from selling assets such as shares and established investment properties (‘capital gains’) will no longer receive the 50% CGT discount. To understand the changes, let’s start with how the system has worked since 1999.

Say you bought an investment property for $500,000, then sold it 10 years later for $900,000. Your nominal ‘capital gain’ is:

$900,000 − $500,000 = $400,000

Because you held the asset for more than 12 months, the CGT discount applies:

$400,000 × 50% = $200,000

That $200,000 is taxed at your

marginal rate.

From 1 July 2027, capital gains will be adjusted for inflation (so only real gains are taxed), with a minimum effective tax rate of 30%. Let’s update the earlier example:

You buy an investment property in 2029 for $500,000, then sell it 10 years later for $900,000. Your nominal ‘capital gain’ is the same – $400,000.

If we assume that inflation over the decade was 3% per year, the ‘indexed cost base’ of your property becomes:

$500,000 × (1.03)10≈ $672,000

So, your real capital gain is calculated like this:

$900,000 – $672,000 =$228,000

That $228,000 is added to your income and taxed at your

marginal rate. However, if this results in an effective tax rate below 30% of the total gain, the tax is increased to reach that minimum.

Transitional rules mean gains are split at 1 July 2027, with earlier gains taxed under the old system and later gains under the new rules. So, for the

approximately 50,000 privately owned rental properties already owned by Tasmanians, any capital gains earned in the years before the new rules kick in will be taxed under the old system.

It’s important to note that the family home remains exempt from CGT.

What about negative gearing

The changes to negative gearing are perhaps more significant. From 1 July 2027, if your investment property makes a loss (i.e., your mortgage repayments and other costs are higher than any rental profits), you won’t be able to use that loss to reduce the tax you pay on your salary or other income. This effectively increases the cost of owning an investment property, especially for high income earners.

However, the negative gearing changes will be ‘grandfathered’. This means that investment properties bought before Budget night aren’t affected – which limits the impact of the change. A more ambitious approach, which we developed and modelled as part of a national

2018 study, would have been to limit the deduction landlords can claim to $20,000 per year for investment properties bought prior to Budget night. This would reduce the tax benefit to about 15% of existing landlords with large property portfolios without affecting ‘mum and dad’ investors.

Critically, the CGT and negative gearing changes target existing properties. Investors in new builds retain full access to negative gearing, and the option to choose between the new indexed system or the old CGT discount – in most cases, the latter will be the better option. This is aimed at channelling investment toward new housing supply.

What the changes might mean for the housing crisis

Having worked on housing and tax policy for twenty years, we think these reforms are an important, albeit overdue, step in the right direction. Based on

our earlier research (backed up by more recent studies from

the Grattan Institute and Treasury modelling for the Budget), the changes will marginally improve housing affordability. Government modelling suggests that house prices will continue increasing over the next couple of years, but by around 2% less.

The downside of slower house price growth is that according to

the Government, it will mean 35,000 fewer dwellings will be built over the next decade. This is because slower house price growth due to the reforms will make building new houses a bit less attractive. However, the Government argues that this will be offset by building 65,000 additional dwellings using the new Local Infrastructure Fund.

The changes will rebalance the market in favour of those buying homes to live in (‘owner-occupiers’) because they will face less competition from property investors now that generous tax concessions are being wound back.

The Government is projecting that as a result, an additional 75,000 people will become homeowners over the next 10 years.

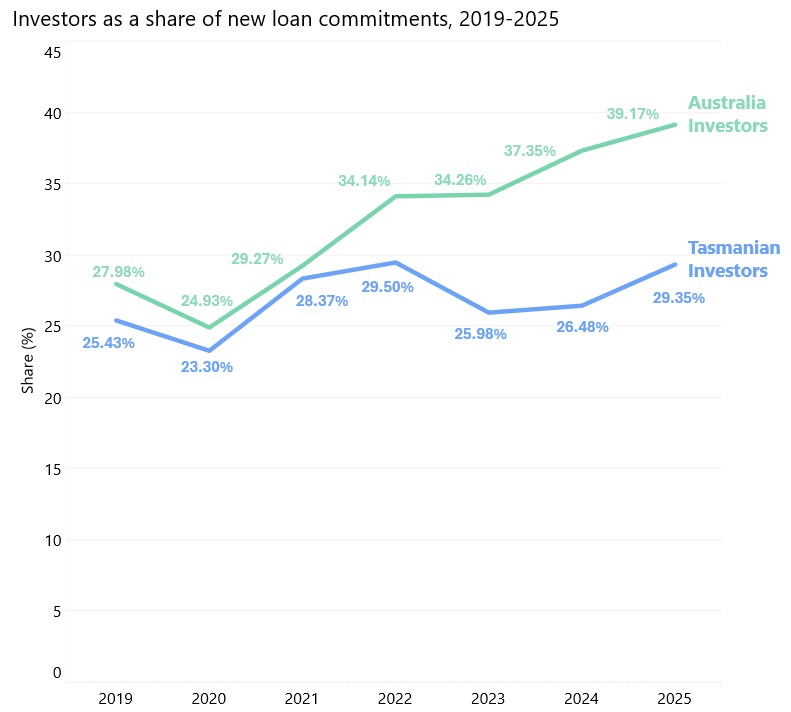

In Tasmania, the effects are likely to be more muted than on the mainland. This is because we have a lower share of property investors.

ABS data shows that in 2025, investors made up 29.4% of new loan commitments to buy dwellings in Tasmania, while the national figure was 39.2%.

The property lobby has argued that pushing investors out of the market will reduce the supply of rentals. But the homes themselves won’t vanish – if they go to an owner-occupier,

that’s one less person competing for a rental.

Of course, many renters won’t be able to buy a home regardless of these reforms, particularly those on lower incomes. To avoid leaving vulnerable Tasmanians further behind, we also need targeted rental assistance and sustained investment in affordable housing.

A less prominent but potentially significant tax change also designed to improve equity is the new minimum 30% tax rate on distributions from discretionary family trusts. This will affect an

estimated 1 million-plus trusts across Australia from 1 July 2028. For Tasmanian small business owners and farming families who rely on trust structures, this change warrants close attention – something we’ll return to in a future article.

Looking ahead

Overall, the reforms will help address the housing crisis but won’t solve it. We need more supply, which is proving to be a challenge across the country. Retaining tax exemptions for investment in new homes is a step in the right direction. We also need to ramp up ‘build to rent’ and other innovative models that ‘crowd in’ private investment for construction – particularly of medium-density housing.

The 2026 Federal Budget represents a step towards addressing a housing crisis caused by 25 years of policy neglect and failure. We now need to focus on building affordable housing and rebuilding communities.

This was originally published in The Mercury in May 2026 as an op-ed, but as part of this PIMBY Bite we've included the evidence behind it, as well as charts and more detail to help further explain the topic.

.png)

.png)